Liquid cooling retrofits can cost roughly 80% less than new AI-ready data centre builds

3 min read- Liquid cooling is becoming necessary for high-density AI and HPC workloads as rack power densities rise beyond the practical limits of air-cooling systems. The report highlights a threshold effect around 40kW per rack and points to AI rack roadmaps moving towards 200kW+ per rack.

- Retrofitting can be significantly cheaper than new build on headline capex – around USD2 million per MW for a liquid cooling retrofit versus upwards of USD11 million per MW for greenfield liquid-cooled capacity – but hidden costs can materially change the investment case.

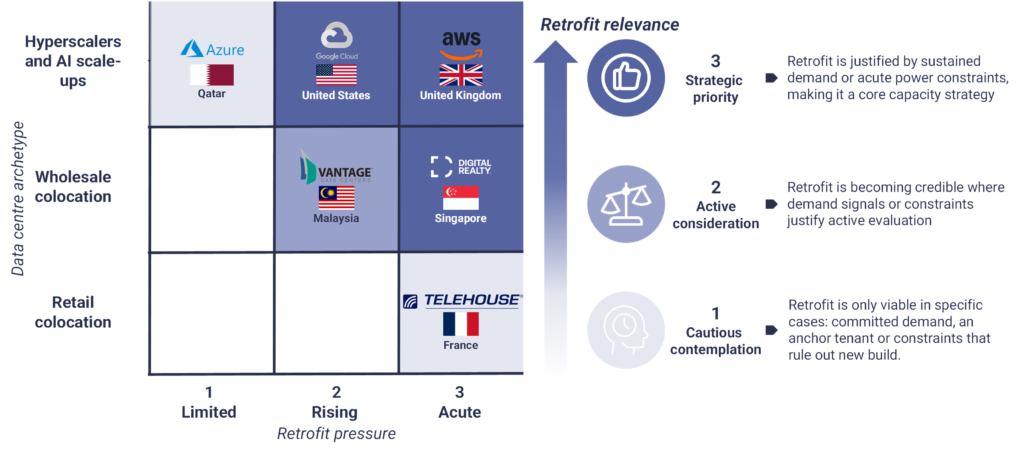

- Retrofit pressure is highest where strong AI/HPC demand coincides with power or permitting constraints. In those markets, secured power in existing facilities can become too valuable to give up.

- Operator archetype matters. Hyperscalers and AI scale-ups can move earlier because they can underwrite demand internally, while wholesale and retail colocation providers need stronger customer commitments, lease certainty and migration plans before upgrading live facilities.

LONDON – 28 May 2026 – Data centre operators are under growing pressure to retrofit existing facilities for liquid cooling as AI and high-performance computing (HPC) workloads push rack densities beyond the practical limits of air cooling, according to a new STL Partners report, The retrofitting roadmap: An evolution of liquid cooling.

The research finds that liquid cooling retrofits can cost around USD2 million per MW, compared with upwards of USD11 million per MW for new greenfield liquid-cooled builds. This makes retrofit a potentially faster and more cost-effective route to AI-ready capacity in markets where power, permitting and land constraints are slowing new construction.

However, STL Partners cautions that retrofit is not a universal answer. Liquid cooling conversions are operationally complex and disruptive, with risks around customer workload migration, downtime, lost tenancy revenues and legacy infrastructure constraints. The report introduces a retrofit viability framework to help operators determine whether retrofit should be treated as a cautious option, an active consideration or a strategic priority.

“AI demand is changing the economics of data centre cooling. Retrofit can look very attractive on headline capex, especially where operators already hold scarce power, but the real question is whether the customer demand, physical asset and operational plan are strong enough to justify the disruption,” said Alice Awdry, Consultant at STL Partners and author of the report.

STL Partners recommends that operators evaluating retrofit use a structured decision process: assess retrofit pressure, test the quality of customer demand rather than volume alone, define an archetype-specific trigger point for action, select cooling vendors as strategic partners, and treat retrofit as an ongoing operational programme rather than a one-off upgrade.

“Operators should not retrofit simply because liquid cooling is the direction of travel. They need a clear trigger point, a retrofit-ready asset and a plan for live-site risk management. The winners will be those that combine demand certainty with disciplined execution,” added Awdry.

When does liquid cooling retrofit become a strategic priority?

Source: STL Partners

Access the full report here.

For media enquiries, click here to get in touch with our team.

STL Partners is a leading research and consulting company that focuses on the telecom industry and adjacent markets by helping telcos and their partners innovate, grow and stay ahead of the competition.