Download

Listen

TM Forum’s Innovate Asia took place for the third time in Bangkok on 24-26 November 2025. This article gives a bird’s eye view of where the industry is at on its journey of network autonomy from Level 0 to Level 5 (L0-5), with a focus on the RAN.

Like the counterpart events in Copenhagen (DTW Ignite) and Dallas (Innovate Americas), Innovate Asia is an opportunity for the telco industry to share best practice and take stock on progress achieved in the preceding 12 months around three main missions: composable IT and ecosystems, AI and data innovation, and Autonomous Networks (AN).

This article reviews progress of AN in the RAN, where mobile operators spend most of their opex and capex and where many of the autonomy initiatives are taking place.

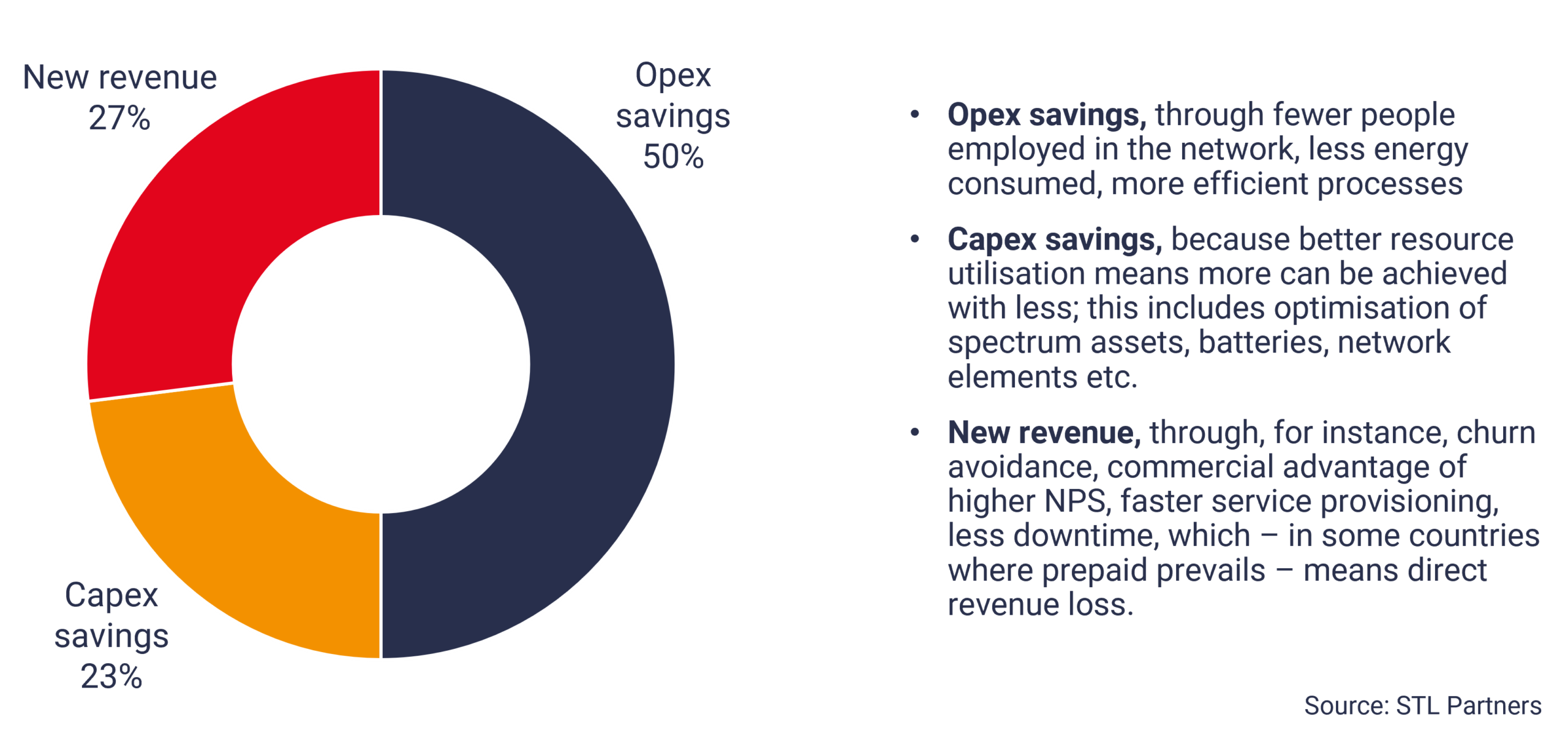

Before we dive into our topic, let me set the scene with an excerpt from STL Partners’ research which assesses the financial value of analytics, automation and AI (A3) in telecom operations. It is the output of a model which identifies 44 processes in an average converged operator’s network and estimates the impact of bringing more intelligence and automation into these processes.

The key messages of this research are clear: for an average operator, the impact in terms of money saved/money gained is equivalent to 5% of annual revenue, with the following main breakdowns:

So, it is important for telcos to invest in autonomous solutions in their networks – access in particular – and doing so will condition their long-term ability to: keep costs down as networks become more complex; spend less time operating their infrastructure; and focus their attention on drawing value out of it.

TM Forum’s autonomy efforts in the RAN have centred on three so-called high-value scenarios (HVS) where operators stand to benefit the most from autonomy and therefore get an adequate return on their investment: RAN fault management, RAN quality optimisation and RAN energy efficiency optimisation.

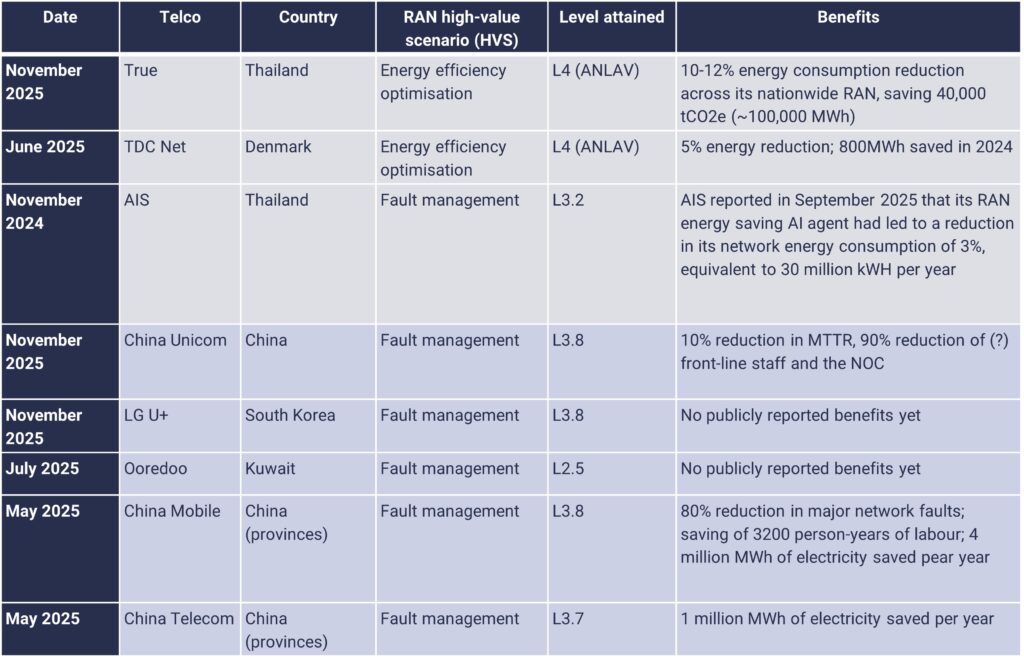

Until June 2025, telcos tended to use TM Forum’s guidelines to self-assess their autonomy status and map their journey through the levels. At DTW Ignite 2025, TM Forum launched a validation service (ANLAV) whereby it, as a third party, independently assesses telcos’ autonomy level in specific domains. At Innovate Asia, TM Forum awarded ANLAV certifications to 12 telcos, most of them Asian, putting the region well and truly in the lead on the network autonomy front.

In the table below, we provide the latest scores on the doors for RAN autonomy in the three aforementioned scenarios, listing operators with ANLAV certificates first (white cell background), followed by telcos for which self-assessment scores only are available (grey cell background).

‘Scores on the doors’ for RAN autonomy HVS (from multiple sources)

It is worth noting that although much has been achieved, as reflected by the autonomy levels attained by the operators listed in the table above and by the fact that the AN mission now counts almost 4 folds of industry partners in 2025 compared with that in 2020, some L4 self-assessments may project an inflated picture of progress, since they may only concern small-scale deployment verification for single scenarios and individual features.

Industry discussions during Innovate Asia 2025 also identified several ways in which the ANLAV certification may be made more mature, we list four main ones here:

- First, in terms of evaluation metrics, adding quantifiable key metrics to the evaluation system is one of the ways to improve accuracy. For instance, introducing Key Capability Indicators (KCI) and Key Effectiveness Indicators (KEI) will enable operators to more precisely measure the operational value and commercial outcomes brought by autonomous networks.

- Each high-value scenario (HVS) may be broken down into smaller sub-scenarios (from 3 to 6) on which autonomy can be evaluated independently of each other.

- An iterative process of evaluation, gap identification, improvement solution development, and solution implementation would help operators continuously enhance network automation and intelligence.

- Finally, when it comes to self-assessment, telcos should strive to apply professional, objective and transparent criteria. In order to so do, they can leverage other mature reference processes that peers have adopted with good results, like for instance the P3 evaluation test, to identify their own shortcomings and gaps with industry benchmarks.

While a specific autonomy level is a useful marker to identify pioneering telcos, it is the business benefits that autonomy brings which should command attention. Autonomy projects are far-reaching transformation endeavours, both from an organisational and technical point of view, requiring high levels of stamina and investment and only justifiable if they deliver definite business value. It is by demonstrating and publishing their own success stories that leading telcos can encourage the rest of the industry to follow in their footsteps, creating stronger momentum, which will benefit the entire ecosystem.

Of the benefits mentioned in my previous table, most relate to efficiencies. KPIs measuring new revenues directly attributable to increased autonomy levels are difficult to come by. In that context, however, it is worth mentioning China Telecom’s 5G-A premium ‘network rights’ plan, whereby the RAN ‘senses’ crowded environments (public transport, but also concerts or sport events where people are likely to live-stream) and the end users receive a prompt offering them the option to pay a premium for temporary QoS network upgrades. Such offerings are only possible with highly autonomous networks and systems.

Finally, it would be difficult to write a blog about network autonomy without touching on AI agents. We saw examples at Innovate Asia of AI agents assisting humans in their network tasks: in the field and in the NOC, by rapidly retrieving information from multiple sources through text or voice prompts.

When it comes to multi-agent systems (MAS) to support RAN autonomy, they currently have not gone beyond the stage of R&D or PoCs. Yet MAS make sense in the RAN for different reasons. For example, they would handle conflicting priorities (e.g. the energy saving agent wants to reduce energy consumption, but the customer experience agent doesn’t want capacity or coverage to be affected) better than single agents that tend to prioritise one KPI over another. Consequently, if each individual agent is confined to its own domain, this contains the impact of any harmful actions to a relatively limited scale compared with a more far-reaching single agent.

Twelve months is not normally a long time in the telco world, but AI has definitely upped the pace of transformation. It will be interesting to see how agentic AI continues to accelerate network autonomy at the next iteration of Innovate Asia.

Do you want to know more about our research in this area?

Strategies for telco infrastructure in an AI world: Part 1

In this article, we asses three AI-driven connectivity opportunities which telcos can monetise

5G standalone: Has the party ended just as it began?

This article examines when, if ever, 5G standalone adoption will become widespread. We look at the insights from our Telco Cloud Deployment Tracker

AI in networks: Top 10 themes

In this article we take a look at the ten key themes discussed at three Futurenet panels on AI in networks.