Download

Listen

This article, kindly supported by Airedale, explores when liquid cooling retrofits make commercial sense, showing why the decision depends on HPC pricing, facility fill, market constraints and disciplined execution.

Why retrofit is rising up the data centre agenda

AI and high-performance computing are changing what data centres need to support. As GPU-intensive workloads push rack densities higher, many facilities are reaching the practical limits of traditional air cooling. The challenge for operators is that demand for high-density, power-intensive capacity is growing faster than new facilities can be built. Greenfield sites may be the strategic ideal for liquid-cooled workloads, but power constraints, permitting delays and long development timelines mean they cannot always arrive quickly enough. This is making retrofit a more attractive option: a way to derive more value from existing powered assets and convert them into capacity that can support the next wave of AI and HPC demand.

However, retrofit should not be treated as a simple cooling upgrade. Converting an existing data centre for liquid cooling can require major changes across mechanical, electrical and plumbing systems, power distribution, structural readiness, cabling routes, thermal design and operational processes. The complexity increases further when the facility remains live, as operators will need to migrate workloads, phase works hall by hall, protect customer uptime and manage risks such as leaks, power disturbances, dust, vibration and disruption during installation.

This means the headline cost of retrofit only tells part of the story. While STL Partners’ research found that a liquid cooling retrofit costs around US$2 million per MW, compared with upwards of US$11 million per MW for new greenfield liquid-cooled capacity, the commercial case depends on much more than capex. Operators also need to account for hidden costs: downtime risk, lost tenancy revenues, workload migration, redesign, compliance work, contractor premiums, contingency and the opportunity cost of converting what is usually still revenue-generating air-cooled space. These factors can materially change the return profile.

Finding the price point where retrofit pays off

The commercial case for a retrofit to liquid-coooled capacity depends on whether the upgraded capacity can generate enough additional value to justify the disruption and investment involved.

To test this, we used STL Partner’s new Retrofit ROI Calculator to model a 60 MW wholesale data centre retrofit scenario,[1] exploring the point at which converting existing air-cooled capacity for liquid-cooled HPC workloads becomes financially attractive. The model compares the cost of retrofitting against the potential uplift from selling upgraded capacity at higher HPC-ready pricing. In other words, it asks a simple question: what price premium does liquid-cooled HPC capacity need to command before retrofit makes sense?

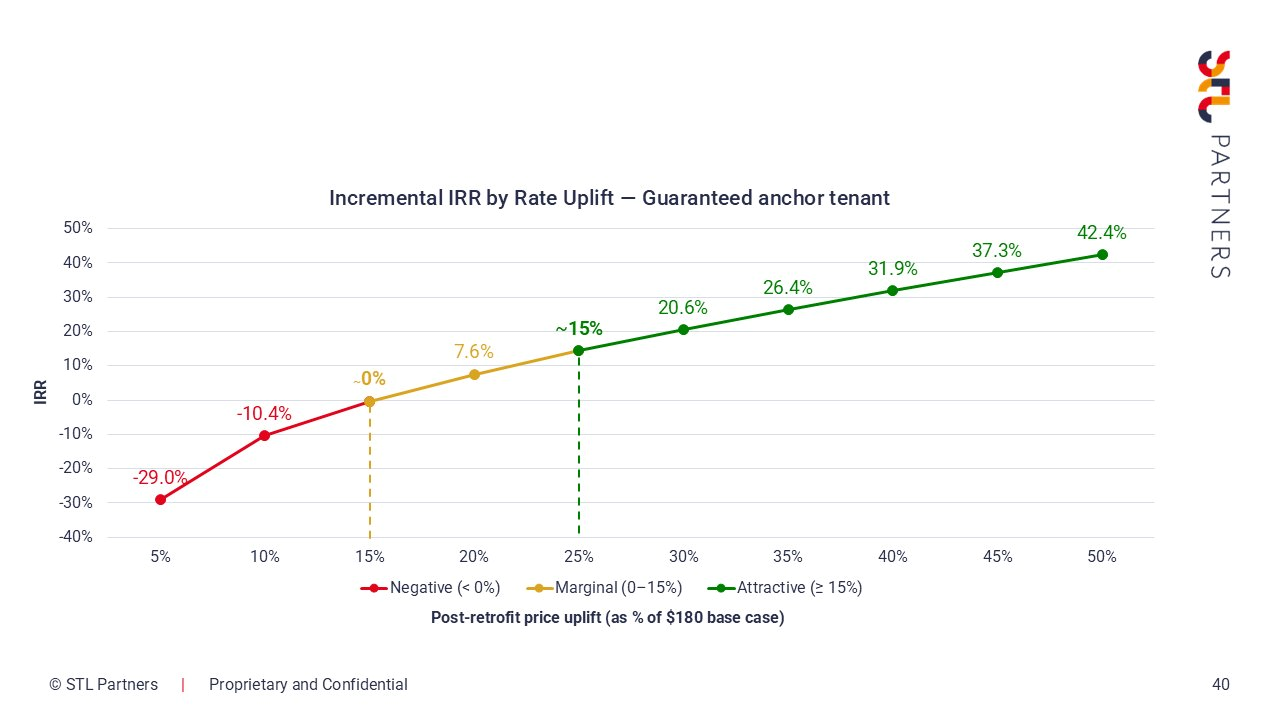

Retrofitting with a guaranteed anchor tenant

Our initial scenario assumes the operator is retrofitting with a guaranteed anchor tenant already in mind.The chart shows how incremental IRR (Internal Rate of Return) changes as the post-retrofit price uplift increases versus a US$180/kW/month base case for non-upgraded air-cooled capacity.

Source: STL Partners Retrofit ROI Calculator

At small price uplifts, the retrofit does not generate enough incremental value to justify the investment. At around a 15% price uplift, returns move roughly to breakeven, suggesting this is the minimum threshold at which the retrofit positively impacts value. The model suggests that the retrofit only becomes commercially compelling once liquid-cooled HPC capacity can command a price premium of around 25% or more. STL Partners research has found that, in mature markets, liquid-cooled HPC capacity can regularly command price premiums of around 20–30% over traditional data centre space, making this a realistic post-retrofit uplift target for operators. At this point, incremental IRR reaches approximately 15%, moving the project into attractive territory – a range usually deemed as an ‘attractive investment’ by infrastructure investors.

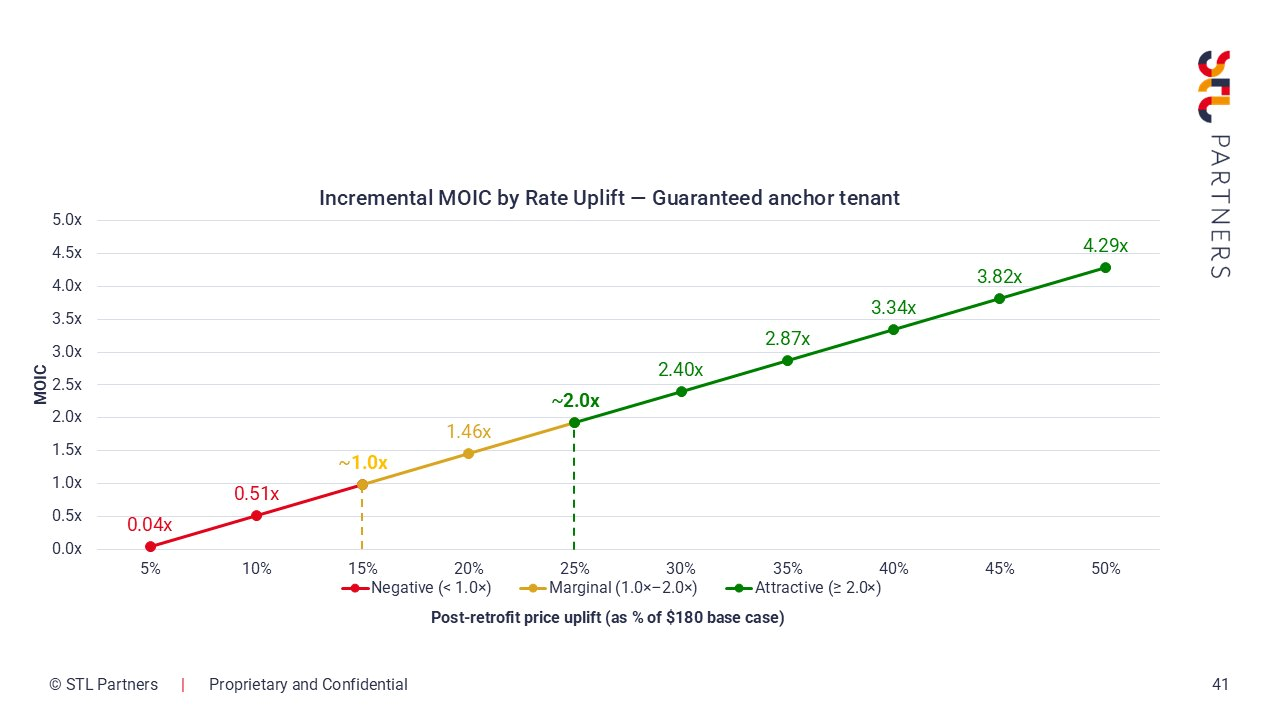

The MOIC (Multiple on Invested Capital) view tells a similar story, but frames the business case in terms of cash multiple rather than annualised return.

Source: STL Partners Retrofit ROI Calculator

Under the guaranteed anchor tenant scenario, the retrofit begins to recover the investment at around a 15% price uplift, where MOIC reaches approximately 1.0x. The retrofit starts to look meaningfully attractive at around a 25% uplift, where MOIC reaches approximately 2.0x. This means the operator is generating roughly twice the invested capital over the modelled period, assuming the upgraded capacity is filled by the anchor tenant.

This modelling reinforces a key point: retrofit economics cannot be assessed on cost alone. Although retrofitting can be materially cheaper than building new liquid-cooled capacity, the business case depends on whether operators can monetise the upgraded capacity at sufficiently high HPC-ready rates. In markets where demand is strong, power is constrained and customers are willing to pay for near-term high-density capacity, retrofit can move from marginal to highly attractive. Where those conditions are absent, the same investment may struggle to clear the required return threshold.

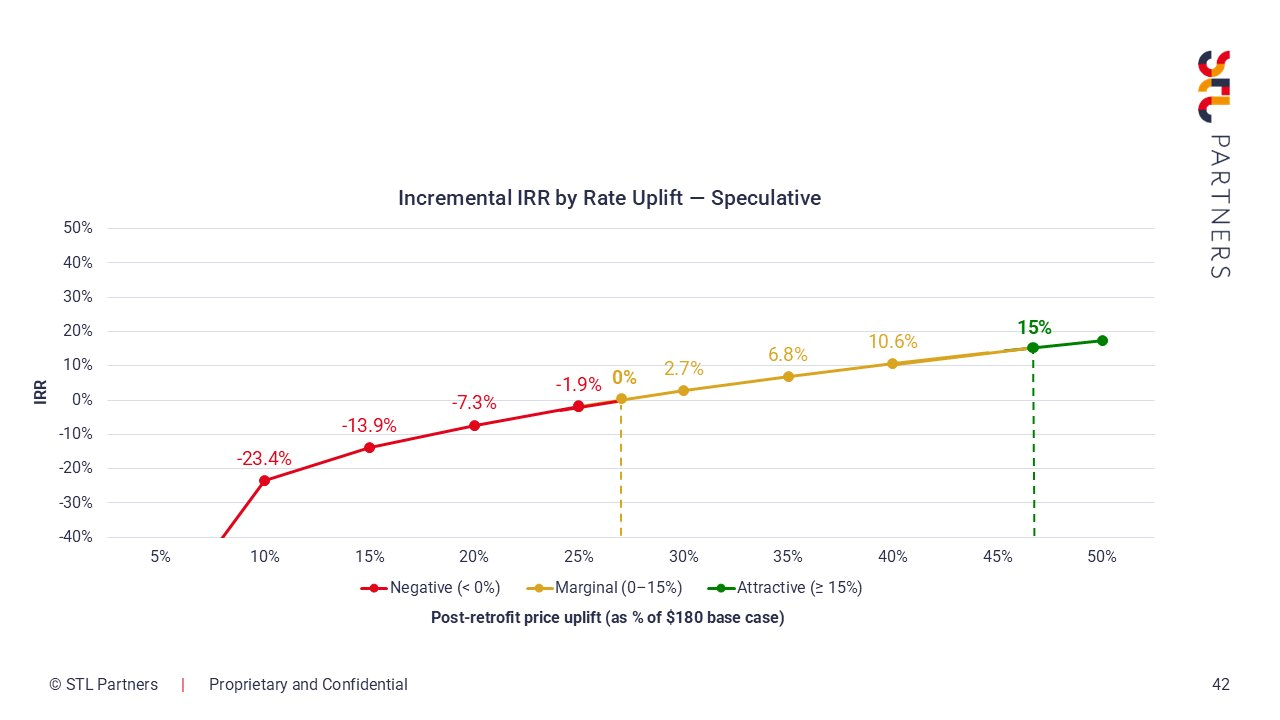

Retrofitting speculatively

The second scenario removes the comfort of a guaranteed anchor tenant. Instead, the operator retrofits speculatively: investing ahead of committed demand, with the expectation that the upgraded facility can be filled over time at HPC-ready rates. This materially changes the investment case. Without a secured tenant, the operator faces weaker financing terms, greater revenue uncertainty and a longer ramp-up period before the upgraded capacity is fully monetised. The project may still be worthwhile, but the margin for error becomes much narrower.

Source: STL Partners Retrofit ROI Calculator

The IRR profile reflects this. In the speculative scenario, returns remain negative until roughly a 28% price uplift, compared with around 15% in the guaranteed anchor tenant case. The project does not reach the attractive threshold of around 15% IRR until approximately a 47% price uplift. While this level of premium is possible in certain markets — JLL notes that AI-optimised facilities can command lease rates up to 60% higher than traditional data centre space — it should only be assumed where demand for AI-ready capacity is acute, power is constrained and customers need capacity quickly.

This explains why operators are unlikely to retrofit speculatively except in highly selective circumstances. The commercial case requires strong conviction that local HPC demand will materialise, that customers will pay a substantial premium for liquid-cooled capacity, and that the facility can be filled quickly enough to avoid returns being eroded by underutilisation. In most cases, retrofit is far more defensible when anchored by committed demand, a major lease event or a clear customer requirement rather than by a general expectation that AI demand will eventually arrive.

Retrofit only works where demand and power constraints align

In both scenarios, operators rely on confidence that upgraded liquid-cooled capacity can be filled, and filled at the right price. To help operators assess this, STL Partners has produced a Retrofit Viability Framework that evaluates where retrofit is most likely to make strategic sense. The framework shows that retrofit is most compelling where strong AI/HPC demand coincides with constrained access to power, land or permits.

Where power is more readily available, the retrofit case becomes less clear. If operators can meet demand through new AI-ready facilities, greenfield development will often remain preferable to converting a live site. This is why the framework assesses both market demand and power constraints when determining whether retrofit should be treated as a cautious option, an active consideration or a strategic priority.

Strong execution protects the retrofit business case

Execution is the final test of whether retrofit value can actually be realised. Even where pricing, tenancy and market conditions support the investment case, poor planning can quickly erode returns through delays, disruption and cost overruns.

As discussed in STL Partners’ retrofit execution checklist, liquid cooling retrofit is not simply a cooling upgrade. It requires coordinated changes across power distribution, structural capacity, thermal design, customer migration and live site operations. Operators need to assess whether the asset is genuinely retrofit-ready, including power availability, floor loading, cabling headroom, pipework routes and the right cooling strategy and vendor for the target density. In live facilities, execution must then be tightly controlled. A retrofit that looks attractive on paper can quickly become value-destructive if technical due diligence and delivery discipline are not in place.

Conclusion

Our modelling shows that retrofit can be a powerful route to AI-ready capacity, but only when the commercial, market and execution conditions align. Operators need confidence that upgraded liquid-cooled capacity can be filled at a sufficient HPC premium, in markets where power constraints make existing assets especially valuable, and with enough technical discipline to avoid delays, disruption and cost overruns. In short: retrofit is not a default response to AI demand — it is a selective strategy for operators that can prove the price, fill the facility and deliver the upgrade safely. For more detail, read our full report.

Looking for advisory services in data centres? Schedule a call.

Download the data centre insights overview pack

Download the data centre insights overview pack

Get a concise, practical summary of the data centre market: the impact of AI and sovereign strategies, the differentiators that win in a crowded landscape, and proven frameworks for market entry, channel partnerships and customer acquisition—backed by case studies and sample deliverables.

Five things we learned at Datacloud Global Congress 2026

We were at Data Cloud Congress 2026 in Cannes last week to evaluate the key narratives among data centre operators, investors and vendors.

Key takeaways from the launch of the Quantum Infrastructure Council

STL Partners attended the launch of QIC to explore what it will take to deploy

quantum technologies in real-world data-centre environments.

The EU’s AI Gigafactory Initiative: What it means for digital infrastructure?

The EU’s €20 billion AI gigafactory initiative will fund up to five large-scale AI compute facilities, each designed to support frontier model training with more than 100,000 advanced AI processors.

Five things we learned at Datacloud Global Congress 2026

We were at Data Cloud Congress 2026 in Cannes last week to evaluate the key narratives among data centre operators, investors and vendors.

The hidden economics of liquid-cooled data centre retrofits

This article, kindly supported by Airedale, explores when liquid cooling retrofits make commercial sense, showing why the decision depends on HPC pricing, facility fill, market constraints and disciplined execution.

Key takeaways from the launch of the Quantum Infrastructure Council

STL Partners attended the launch of QIC to explore what it will take to deploy

quantum technologies in real-world data-centre environments.